A Central Bank Digital Currency, [CBDC] is digital money that is backed by, and circulated by, a central bank.

These can be used in the same way as regular money but are created on a distributed ledger. This is where the “digital” part comes into play, but make no mistake, this has nothing to do with a cryptocurrency. They share none of the core values cryptocurrencies (i.e. decentralisation, transparency, publicly verifiable and immutable transactional record, etc.)

It is estimated that more than 80% of central banks around the world are considering launching a CBDC or have already done so.

This is a reason to explore the CBDCs topic in more detail and find out what exactly are we facing in the near future as CBDCs gain more traction and why I say in my title, that these are in fact dangerous, or in the very least – problematic.

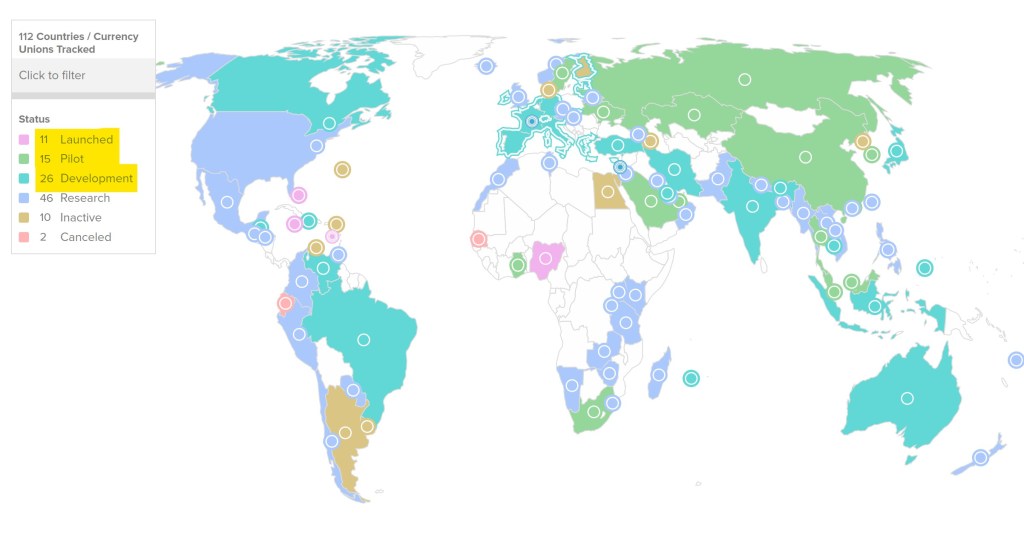

According to the latest statistics by Atlantic Council CBDC tracker, at present 105 countries, representing over 95 percent of global GDP, are exploring a CBDC.

In comparison, back in May 2020, only 35 countries were considering a CBDC.

A new high of 50 countries are in an advanced phase of exploration (development, pilot, or launch).

10 countries have fully launched a digital currency, with China’s pilot set to expand in 2023. Jamaica is the latest country to launch a CBDC, the JAM-DEX. Nigeria, Africa’s largest economy, launched its CBDC in October 2021.

Many countries are exploring alternative international payment systems. The trend is likely to accelerate following financial sanctions on Russia. There are 9 crossborder wholesale (bank-to-bank) CBDC tests and 3 cross-border retail projects.

Of the G7 economies, the US and UK are the furthest behind on CBDC development. The European Central Bank has signaled it will aim to deliver a digital euro by the middle of the decade.

19 of the G20 countries are exploring a CBDC, with 16 already in development or pilot stage. This includes South Korea, Japan, India, and Russia. Each has made significant progress over past six months.

The financial system may face a significant interoperability problem in the near future. The proliferation of different CBDC models is creating new urgency for international standard setting.

3 Reasons Why CBDCs Are Problematic

- CENTRALISED

They are centralised, making them the perfect tool to exercise censorship.

Freezing of accounts and access to all of your money can be instant and even easier than it is already. - PROGRAMMABLE

CBDCs are programmable money – similar to food coupons, we can be forced to spend them on certain goods or services, thus restricting our personal liberties. This is an article - END OF PRIVACY

Government can trace everything you buy or sell, even if you just lent a fiver to your friend – nothing will be private anymore.

CBDCs offer great transparency but only to those who control the database, unlike cryptocurrencies, which offer publicly accessible and verifiable database.

With this in mind, and the obvious advance of digital money, a recent report from PwC highlights some of the biggest challenges they will face in coming years.

The 2022 PwC CBDC Global Index analyses and ranks the leading retail and wholesale CBDC projects. The Index evaluates the current stage of CBDC project development also taking into account central bank opinion and public interest.

The leaders in CBDCs according to that report, are Central Bank of Nigeria’s (CBN) eNaira (the first CBDC in Africa) and the Sand Dollar, issued by the Central Bank of the Bahamas as legal tender in October 2020, making the Bahamas the first country to launch a CBDC, while China became the first major economy to pilot a CBDC in 2020 with the Digital Yuan, and as of March 2022 pilot programs are running in 12 cities, including Beijing and Shanghai.

According to John Garvey, Global Financial Services Leader at PwC, the report outlines the importance and greater utility that CBDCs offer. He seems to completely ignore any of the factors that make CBDCs problematic and concludes the following:

“One thing that is clear, lowering the cost of payments in an economy provides value throughout the economy and for citizens. If CBDCs can ultimately enable more efficient payments, that will benefit everyone.”

(https://www.pwc.com/gx/en/news-room/press-releases/2022/pwc-cbdc-global-index-2022.html)

More than 88% of CBDC projects, at pilot or production phase, use blockchain as the underlying technology.

Whilst a blockchain is not always necessary to create digital tokens, blockchain technology brings several benefits to CBDC developments. Namely:

• Integrated platforms built by design to share value and transfer ownership in a secure way, which is key to supporting digital money;

• Smart contract programmability, supporting CBDC as a new form of programmable monetary instrument that could trigger automatic payments

based on pre-programmed conditions;

• Transparent audit trails;

• Configurable confidentiality features;

• Increasing interoperability with other digital assets

through atomic swaps.

At face value, this seems alright, there’s a mention of the word “transparency” which usually implies a positive connotation. However, the transparency here is really only one-sided. Being centralized, these digital currencies will allow full transparency only to the ruling party – the one that controls the ledger. This will not be public access like we see with distributed ledger technology (such as most cryptocurrencies).

The problem with giving away all privacy (in this case, your capital flow) to a centralized power, is that sooner or later, that power is abused. It can be very detrimental to us, should that party choose to implement rules that aren’t popular with the nation (and we’ve seen this happen with Covid mandates for instance).

At this point we can only speculate as to what and how CBDCs can or will be used for, but one thing is for sure.

Should they be allowed to become programmable money, where certain conditions have to be met in order for a transaction to be executed, this will open the door to any number of conditions that will further restrict the liberties of ordinary citizens as to how or when or even how much of their own money they can be allowed to spend on certain goods or services (and even some could have right-out bans).

This to me, presents the biggest threat to citizens and which is why I feel that much more attention needs to be paid to the development of CBDCs and especially the legal framework that will be built around them.

Spread the word about this and don’t forget – once the machine starts rolling, it will be too late. We need to act now, to make sure that when CBDCs are voted in, we put restrictions on what they can do with them and how they program them – this is the least we can do for our own sake.

☝These are my opinions, not financial advice, always DYOR.

📖“Learn Crypto” eBook is the ultimate beginners guide to cryptocurrencies that helps you avoid the mistakes all newbies make when investing in crypto: https://LearnCryptoNow.com

📖“Learn Crypto” eBook is the ultimate beginners guide to cryptocurrencies that helps you avoid the mistakes all newbies make when investing in crypto: https://LearnCryptoNow.com

⚠️ DISCLAIMER ⚠️

The information contained in this video is for informational purposes only. Nothing herein shall be construed to be financial or legal advice. The content of this post reflects solely my own opinions. Purchasing cryptocurrencies poses considerable risk of losses.